Property insurance claims are a …

Below you'll find a list of all posts that have been tagged as “business interruption insurance”

Property insurance claims are a …

Now more than ever, as …

Though high winds can cause …

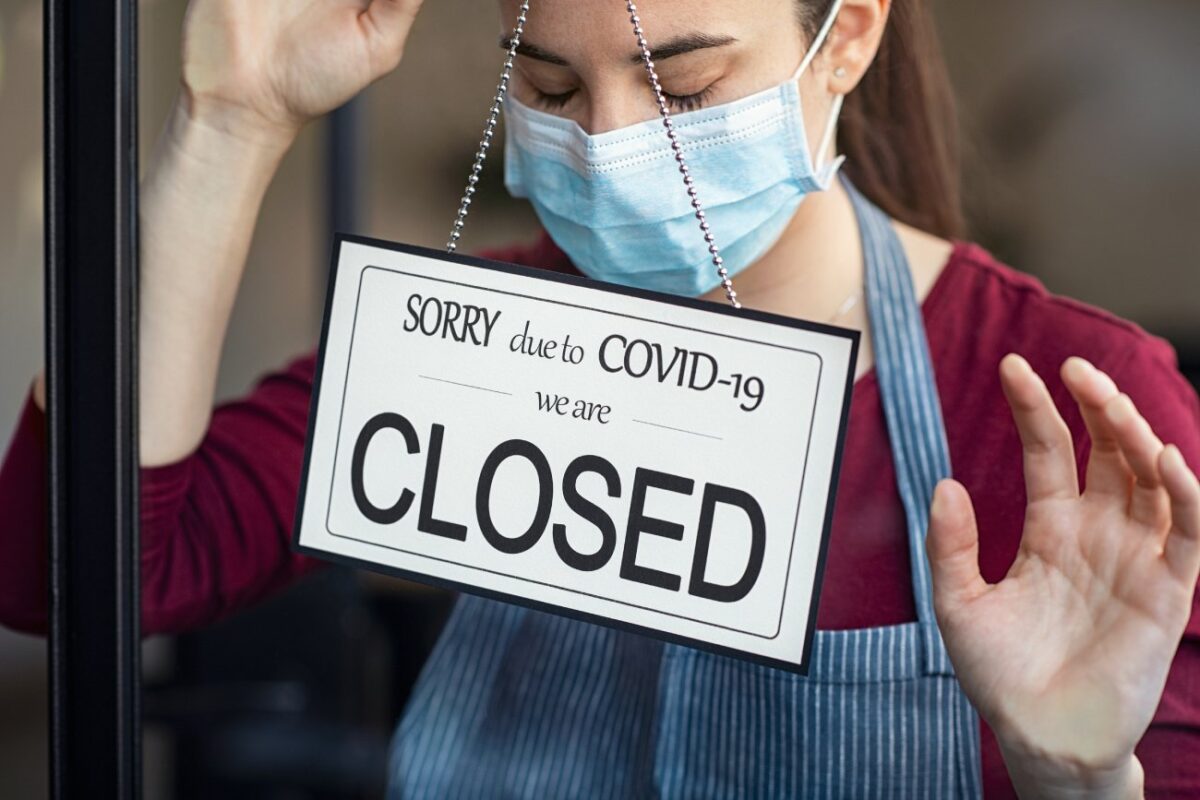

All over the country, business interruption losses are occurring due to the need for people to remain inside their homes. As a result, brick-and-mortar businesses are suffering. Here’s what you can do.

COVID-19 insurance claims denied? Business interruption insurance is created for times like this. If you’ve been paying your premiums, you deserve a payout.

Business owners do a lot …

Miami, Fla., April 2, 2020 …

When you purchase business interruption …